With Whiteshell Provincial Park, Narcisse Snake Dens, and Canadian Fossil Discovery Center, Manitoba lays claim to some of the most exciting road trip destinations in Canada. But driving here is certainly not cheap. Manitobans pay more than the national average for car insurance.

So, short of packing your bags and moving to a cheaper province, what else can you do to lower your monthly Manitoba Insurance bill?

Start with implementing the easy, practical, and effective tips shared in this article. Whether you are buying the mandatory coverage from MPI or additional coverage from a private insurer, these tips will help you shed precious dollars off your premium.

Additionally, we have explained how auto insurance works in Manitoba without any technical mumbo-jumbo, listed all available insurance coverages, and described the licensing process.

So, let’s dive straight in.

How Vehicle Insurance in Manitoba Works

Just like British Columbia and a few other provinces, Manitoba requires its drivers to purchase basic auto insurance through a government-owned corporation, called Manitoba Public Insurance (MPI). However, Manitoba residents have the freedom to purchase additional coverage from private insurance companies or private insurance brokers, besides MPI.

For example, while the basic car insurance offers third-party liability protection up to $200,000, Manitobans can increase the amount to $1 million, $5 million, or even $10 million. Private insurers often offer a better value for money than MPI when it comes to optional coverages, but we recommend evaluating all options concerning Canada and car insurance.

Who Sets Rates

Manitoba has a government-run car insurance market. Manitoba drivers must purchase compulsory auto insurance from MPI. They can’t shop around for basic coverage if they don’t like their premiums.

The Financial Institutions Regulation Branch regulates private insurance companies in Manitoba. In case you want to make a formal complaint against your private auto insurer, submit the complaint form online.

Pure No-Fault System

Manitoba has a pure no-fault system. In simple terms, this means you’ll deal with your insurance company and the other driver with theirs, in case of an accident, and neither of you can sue the other person for damages they have caused.

AWN Auto Parts

Free Shipping On All orders over $1OO auto parts and accessories

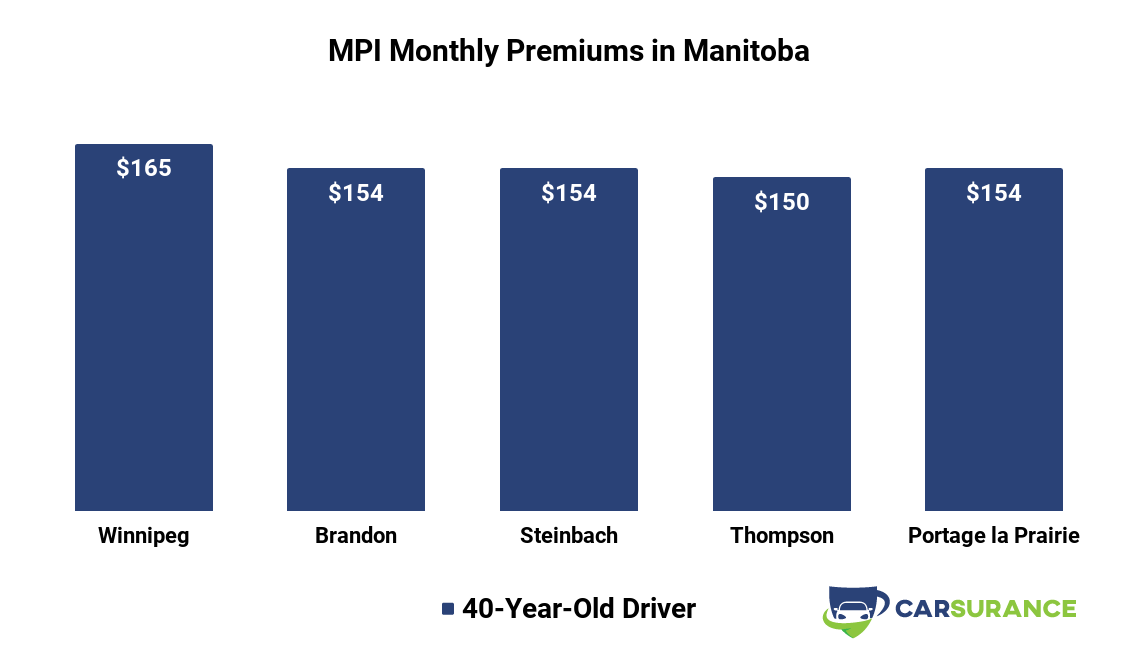

Manitoba Public Insurance Coverage Prices in Major Cities

To verify car insurance rates, we got quotes from MPI. We selected the minimum limit of $200,000 along with a $500 deductible. Our reference driver was a single 40-year-old man with a clean record, driving a 2018 Honda Civic Sedan SE.

Unlike most other provinces, car insurance rates in Manitoba don’t vary that much from one city to another. For instance, the price difference in the costliest and cheapest city for car insurance is just about 9%.

- At $165 a month, car insurance in Winnipeg is more expensive than anywhere else in Manitoba.

- Brandon, Steinbach, and Portage la Prairie emerge as the second-most-expensive cities for auto insurance, with a monthly premium of $154.

- Thompson, at $150 a month, has the lowest premiums.

Which Auto Insurance Coverages Are Available in Manitoba

The following coverages are available in Manitoba.

- Public Insurance — MPI offers mandatory car insurance coverage. It includes liability, uninsured motorist, and accident benefits coverage.

- Private Insurance — Most people buy optional coverages from private Manitoba insurance companies or private insurance brokers. Nonetheless, MPI itself also sells additional coverages. If you want to purchase optional insurance from a private auto insurance company, we recommend that you shop around first. Comparing quotes of several players online doesn’t take too much of your time and can go a long way in helping you get the best bang for your buck.

- No-Fault Insurance — Manitoba operates under a pure no-fault system. Meaning each driver must deal with their auto insurer in the event of a road accident, regardless of fault. Also, Manitoba car insurance rules dictate that you cannot sue the negligent driver for the damages.

- Third-Party Liability Insurance — This coverage protects you when someone gets injured or killed or their property gets damaged in an accident caused by you. This is the only coverage that is mandatory in every Canadian province besides Quebec, though the minimum coverage amount is not the same everywhere. According to Manitoba vehicle insurance laws, every driver must carry $200,000 in third-party liability.

- Accident Benefits — It pays for medical expenses incurred by you after an accidental injury, regardless of fault.

- Uninsured/Underinsured Motorist — It protects you if you and your passengers are hurt in an accident involving an uninsured or underinsured driver or a driver who commits a hit-and-run. This is mandatory insurance coverage in Manitoba.

- Collision Insurance — This is a protection plan that’s included under the mandatory All Perils insurance in Manitoba. It covers the cost of repairing or replacing your car if it gets damaged as a result of a collision with another vehicle or stationary object.

- Comprehensive Coverage — It protects your car against damage or loss caused by external events such as theft, fire, vandalism, glass breakage, and more. It doesn’t cover damage or loss resulting from a collision with another vehicle or object. It’s also a mandatory part of your insurance quote in Manitoba, Canada, since it’s relatively covered under All Perils.

- All Perils — It provides protection against everything covered in Collision and Comprehensive coverage, plus theft by an employee or somebody living with you.

- Emergency Roadside Assistance — This optional coverage can save the day for you when you suffer a mechanical breakdown on the road. Services typically included are fuel delivery, locksmith service, extrication or winching, towing, battery jump-start, and tire replacement.

Minimum Public Manitoba Insurance

It is illegal in Manitoba to drive a vehicle that’s not covered by MPI’s Basic Autopac insurance coverage. The bare-bones minimum coverage includes:

Third-party liability coverage of $200,000

It protects you in case you hurt someone or you damage somebody’s property in a car accident.

The minimum third-party liability coverage that every Manitoba driver needs is $200,000, according to Manitoba Public Insurance website. If someone files a claim that reaches the mandatory limit and involves both bodily injury and property damage, the maximum compensation for the latter will be $20,000.

All Perils Coverage

It provides protection against accidental loss or damage resulting from:

- a collision with another vehicle or an immovable object;

- rolling or tipping over with your car;

- other causes, such as hail, fire, theft, and vandalism.

All perils coverage included in the basic Autopac from Manitoba Public Insurance Corporation is capped at $50,000.

Personal Injury Protection Plan (PIPP)

The mandatory third-party liability coverage also includes PIPP, which reimburses medical expenses due to injury in a road accident, irrespective of who caused the accident. The plan also covers income replacement, caregiver expenses, personal care assistance, permanent impairment, rehabilitation, and catastrophic injuries. PIPP covers all Manitobans who get hurt in an accident either in Canada or the US.

AWN Auto Parts

Free Shipping On All orders over $1OO auto parts and accessories

How Manitoba Auto Insurance Prices Compare to Other Provinces

Drivers in Manitoba have to dig a little deeper than the average Canadian to pay for car insurance. While the national average annual premium is $1,064, Manitoba residents on average pay $1,080 per year. All Perils coverage may be the one to blame. It mandates the relatively expensive collision and comprehensive coverages, which drive the prices up.

What Impacts Auto Insurance Prices in Manitoba

Age and gender don’t affect car insurance rates in Manitoba, but there are several other factors that can impact your premium.

- Where you drive — If you live in a major city, such as Winnipeg, you’ll likely pay more because of high population density. Typically, accident and theft rates are higher in heavily populated areas.

- Car make and model — If you drive a car that’s expensive or costly to maintain, expect to pay more for Manitoba insurance. In general, auto insurers charge more for insuring a new or sports car.

- Driving activity — As a rule of thumb, the more kilometres you drive in a year, the higher the premium.

- Driving history — You can considerably lower your premium by demonstrating safe driving behaviours over a long period of time.

- Discounts — The best way to save on the basic coverage from Manitoba Public Insurance is by availing all discounts available to you. Safe driving discounts, anti-theft device discounts, and low-kilometre discounts can all help you shave precious dollars off your annual insurance bill.

- Insurance coverage — Every driver in Manitoba must buy the mandatory coverage from MPI. In addition to the bare bones, car owners can purchase add-ons from MPI, private insurance brokers, or private insurers. Naturally, the more optional products you tack on your policy, the higher the annual premium.

How to Get The Cheapest Car Insurance in Manitoba

Manitoba drivers pay more than the national average for car insurance, but you can lighten the strain on your wallet by following these time-tested tips.

Shop around

When it comes to basic car insurance, MPI is the only option available to you. But that’s not the case with optional insurance, which you can buy from anyone — a private insurance broker, a private insurance company, or MPI itself. Study our car insurance reviews to determine the best companies for you, and gather quotes from different players and compare them to get the best possible deal.

Bundle your policies

If you use the same insurer for auto and home insurance in Manitoba, you can expect a handsome discount on both.

Ask about discounts

If you’re a member of the Canadian Automobile Association (CAA), a union, a school alumnus, or a large corporation, you might qualify for a discount.

Pay premiums annually

Pay annually instead of monthly, and your insurer is likely to thank you with a dip in your premium.

Install an anti-theft device

Protect your ride with an approved anti-theft device, such as an electronic immobilizer, and see your car insurance Winnipeg premium drop.

Increase your deductible

A deductible is a portion of the car insurance that you must pay before your insurer chips in. A general rule of thumb: the lower the deductible, the higher the premium.

Still, mind you, when you raise the deductible, you’re basically trading a lower premium for less coverage.

A good driving record

Whether you are looking for an affordable Winnipeg car insurance, or you live in another major city, a clean driving record helps lower your costs. In general, the better the driving record, the lower your premium.

Getting a Driver’s Licence in Manitoba

Manitoba has a graduated driver licensing system in place that requires every driver to pass through a 3-step educational program before they can become a fully-licensed driver.

- Learner (L) License

You can get a learner’s license if you are 16 years of age, or 15 years and 6 months if you are registered in a high school driver’s education course, and pass a written test.

Someone with a full license must accompany an L driver whenever they take the wheel. According to the Manitoba insurance act, driving without insurance in Manitoba is an offence; never drive a vehicle that doesn’t have the province-mandated insurance through MPI.

- Intermediate (I) License

After you’ve had an L license for a minimum of 9 months, you can sit for the Learner’s road test. Passing it will take you one step closer to becoming a fully-licensed driver.

- Full (F) License

You will get your full license after you’ve held onto the intermediary license for a minimum of 15 months.

People Also Ask

Manitoba’s average premium is slightly costlier than the average rate. Drivers here shell out $1,080 for auto insurance, which is $16 more than the national average.

Just like Quebec, Manitoba has a pure no-fault system. That is, in the event of an accident, each driver will be covered by their respective insurance company, and neither they nor their insurer can sue the at-fault driver for compensation.

According to the MPIC website, the basic Autopac Coverage includes third-party liability coverage, all-perils coverage, and personal injury coverage.

An abstract of driving record or a driver abstract is basically a printed copy of your driving record. You can obtain a driver abstract from MPI by paying a $10 fee.

As per Manitoba Insurance rules, your driver’s abstract will confirm information from your driving record. This includes name, address, sex, date of birth, eye colour, height, licence effective date, license expiry date, license status, license class, convictions, suspensions, at-fault collision, and more.